- The Conveyor

- Posts

- The Next S-Curve in Solar

The Next S-Curve in Solar

Aditya Dhathathreyan on the current state of the solar industry and how the US can compete.

Gowtham Ramachandran

August 20, 2024

Photo by Manny Becerra on Unsplash

The US, once a pioneer in solar technology, now finds itself in a precarious position - it’s heavily reliant on China for solar.

Chinese firms control over 80% of the global supply chain for silicon solar panels, and China’s share of polysilicon, the core material for the panels, is even higher.

And in recent years, US policymakers have begun to take notice.

They are trying to revitalize domestic solar manufacturing through initiatives like the Inflation Reduction Act.

But China's cost advantages are substantial, with manufacturing costs 20% lower than in the US and 35% lower than in Europe.

Considering China’s overwhelming advantages in the solar supply chain, the US will have to look beyond incremental improvements to regain leadership in the solar industry.

I was curious to learn about the most promising emerging technologies in the solar industry, so I sat down with Aditya Dhathathreyan, who works in the supply chain and power markets team at Aquila Group, to get his perspective.

Aditya has worked in the solar industry for over a decade now. He started his career working for SunEdison and has since held significant roles at Brookfield, Enzen, and Siemens Gamesa. He now works for Aquila Group, based in Singapore, where he is exploring opportunities in the renewable energy sector and expanding data centers.

In this piece, I’ve written about:

The historical context that led to this situation

The current solar manufacturing supply chain

One way the US could compete with China

Let’s dive in 👇

History of Solar

The story of solar begins in the US.

Bell Labs engineer testing a solar cell in 1954. (Bell)

In 1954, Bell Labs developed the first practical silicon solar cell, marking the birth of modern solar power.

Throughout the 1960s and 1970s, the US government and private sector invested heavily in solar research and development, driven by the space race and the need for satellite power systems.

1985 brought another leap forward when researchers at Stanford University demonstrated a solar cell with 25% efficiency.

As the new millennium approached, the solar industry was poised to expand.

In 2000, First Solar opened its manufacturing facility in Perrysville, Ohio, with an annual capacity exceeding 100 megawatts. At the time, it was the world's largest photovoltaic production facility, symbolizing America's commitment to solar leadership.

But despite this early lead, the US gradually lost its competitive edge.

Several factors contributed to this decline:

Lack of consistent policy support: The US failed to maintain long-term, stable policies to support the solar industry.

Focus on short-term profits: Many US companies prioritized immediate returns over long-term investments in manufacturing capacity.

High labor and energy costs: Over time, compared to China, the US faced higher production costs, making it difficult to compete on price.

At the same time, China recognized the strategic importance of the sector and implemented a series of policies to dominate the industry:

Government subsidies: China invested over $50 billion in new PV supply capacity, ten times more than Europe.

Industrial clusters: China established specialized regions for solar manufacturing, enabling innovation and efficiency.

Export-oriented strategy: Chinese companies focused on scaling up production for both domestic and international markets.

Vertical integration: Chinese firms controlled multiple stages of the supply chain, reducing costs and improving coordination.

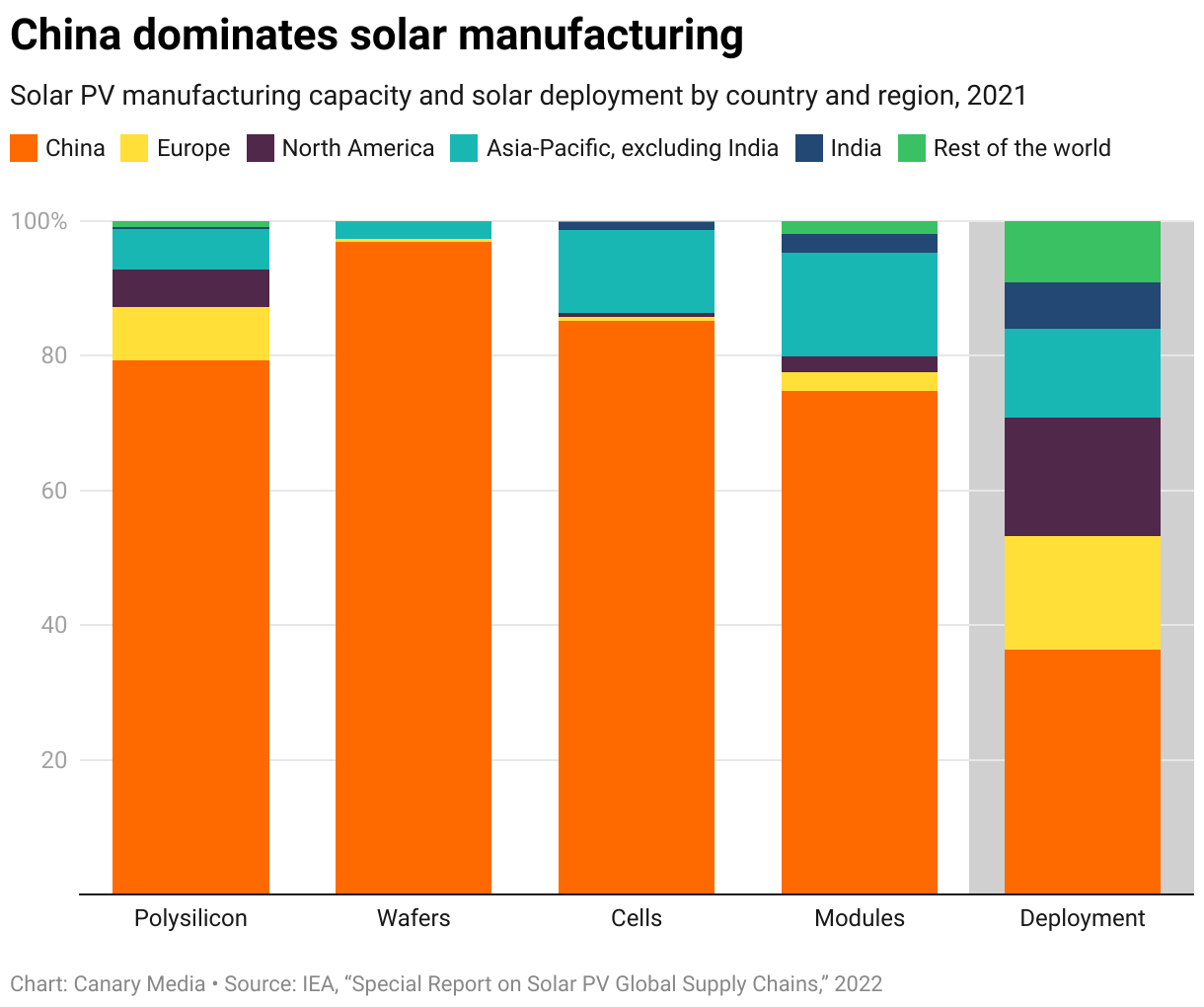

As a result of these efforts, China's share in all manufacturing stages of solar panels has exceeded 80%. Between 2010 and 2020, the global average price of solar modules fell by over 80%, largely due to Chinese manufacturing efficiency and scale.

While this price reduction has accelerated solar adoption worldwide, it has also made it increasingly difficult for non-Chinese manufacturers to compete.

Today’s Solar Supply Chain

Solar Manufacturing Overview

The solar manufacturing process begins with polysilicon production, where quartz sand is refined into high-purity polysilicon. This polysilicon is then melted and formed into ingots, which are sliced into thin wafers.

These wafers undergo cell fabrication, where they are textured, doped to create p-n junctions, and coated with anti-reflective materials to form functional solar cells.

Finally, the solar cells are interconnected and assembled into modules, where they are laminated between glass and a backsheet, framed with aluminum, and fitted with a junction box for electrical connections.

China’s Dominance

This entire process is highly integrated, dominated by Chinese manufacturers at each stage.

Here’s China’s market share across each stage of the solar manufacturing process:

Polysilicon production: 80% market share

Ingot and wafer manufacturing: 95% market share

Cell fabrication: 80% market share

Module assembly: 75% market share

So, why does China have such a dominant position?

It’s because it’s significantly cheaper to manufacture in China compared to other nations.

When China started production in the early 2000s, the government provided significant support through subsidies and favorable policies that helped kick-start the industry.

As China gradually built up their manufacturing capacity, they started vertically integrating by building dominant positions across every stage of the supply chain. This helped them reduce costs even more as their increasing production volumes allowed them to achieve economies of scale.

Besides their scale advantage, Chinese manufacturers also benefit from lower electricity prices, lower wages, and less stringent labor and environmental regulations, compared to other nations.

Aditya pointed out:

"The biggest problem in both the U.S. and Europe is the labor rates. If the labor rates were, you know, much lower, then why would you look offshore for manufacturing?"

As a result, it’s no surprise that China’s manufacturing costs are 20% lower than in the US and 35% lower than in Europe.

How Can the US Compete?

Considering China’s overwhelming advantages in the solar supply chain, the US will have to look beyond incremental improvements to regain leadership in the solar industry.

I asked Aditya for his thoughts on how the US can compete with China.

He said the US is unlikely to compete with China in the current landscape, but the US has a chance if it focuses its efforts on creating the next S-curve in solar technology.

"Imagine that you spend trillions of dollars building a new factory, and then suddenly that factory is no longer relevant to the product it produces because something else has come onto the market.

My personal thought process is focused on domestic R&D.

Of course, the R&D environment is global, and people learn from different companies, but you really need to pump in a lot of focus into R&D and then start manufacturing for your R&D.”

Aditya mentioned several emerging solar technologies during our conversation, including:

Perovskite Solar Cells

Monocrystalline Silicon

Heterojunction Technology

TopCon (Tunnel Oxide Passivated Contact)

Amorphous Silicon

But Aditya was most optimistic about the potential of Perovskite Solar Cells.

"There is a technology called perovskites, which is ceramics. For ceramics, you don't need sand. Ceramics can be made in a furnace where you can control the crystalline structure to capture different spectrums of light. That's the new technology that is going to come. I don't know when it will arrive, but I have been speaking and finding out if perovskites are in commercial production and so on. It will suddenly happen: first, there will be one test site or pilot site. Then, they will start noticing that the efficiencies are good. And suddenly, like China, for example, they will just turn the key and say, 'Yep, we're going to do perovskites."

Perovskite Solar Cells

Perovskite solar cells are a type of solar technology that uses a special material called perovskite to convert sunlight into electricity.

Compared to traditional silicon-based PVs, perovskite solar cells have three key advantages:

Efficiency: They can absorb light across almost all visible wavelengths.

Ease of manufacture: They can be made using simple methods, similar to printing or spray-coating.

Flexibility: They are thin and flexible, which opens up new applications where rigid panels wouldn’t work.

Besides technology advantages, the governments like them as well because the raw materials for perovskites are not scarce; they’re found in many parts of the world. And it only takes a very thin layer of perovskite (between 0.5 and 1 micrometre) to make a solar cell. This saves raw materials and makes them even cheaper.

Current Status

Perovskite cells have been researched for more than a decade.

Initially, they couldn’t match silicon cells in their efficiency at turning light into electricity, and tended to degrade in humid conditions.

But recent laboratory-scale devices have shown remarkable progress in efficiency, increasing from 3.8% in 2009 to over 25% today, which is close to traditional silicon solar cells. In fact, some perovskite-silicon tandem cells have reached almost 30% efficiency.

However, scientists are yet to solve one major problem: durability.

Perovskite cells degrade quickly when exposed to moisture, oxygen, light, heat, or applied voltage. Recent research has shown significant improvements in stability, with at least one report achieving a lifetime of 42 days. But for perovskites to go mainstream, their operational lifetime needs to be at least 20 years.

Who is developing them?

Japan seems to be taking a leading role in developing perovskite technology, spurred by government subsidies and other support.

In fact, the technology was invented by Japanse scientist Tsutomu Miyasaka, and recently, Japanese Prime Minister Fumio Kishida has pledged to make the technology commercially viable in two years.

And many engineers believe Japan has a technological edge, since creating a uniform super-thin perovskite layer requires precise craftsmanship, a strength of Japanese manufacturing.

Meanwhile, the US has many organizations working on the technology as well.

The US Department of Energy's Solar Energy Technologies Office (SETO) supports various projects aimed at increasing efficiency and lifetime while reducing manufacturing costs. Academic institutions like the National Renewable Energy Laboratory (NREL) and the Karlsruhe Institute of Technology (KIT) are also at the forefront of perovskite research.

China is not too far behind either.

Several Chinese companies, including CATL, Renshine Solar and Trina Solar, are actively developing and improving perovskite solar cell technology. In fact, China’s Three Gorges Renewable Group has already launched the world’s first commercial megawatt-level perovskite ground photovoltaic project in Mongolia last year.

Source: China Daily

What’s next?

Perovskite solar panels will fit well into manufacturing supply chains Western nations want to build out. But more research is needed on its durability and reliability before it can be used in utility-scale solar plants.

Even without perovskite, the solar industry is set to cut electricity generation costs by 30% between now and 2030, as silicon cells get more efficient.

But if Western Nations want to play a significant role in the future of solar, they’ll have to find a way to solve the durability problem with perovskite technology, or perhaps an alternative technology that can compete with status-quo silicon-based solar.

Bristol-based analysts Rethink Energy is optimistic about perovskites’ commercial viability though - they believe it’ll make up 100 GW of solar panel manufacturing by 2030 and scale up quickly from there.

Source: Rethink Energy

“Every one of the major silicon PV manufacturers will eventually enter perovskites well before 2030”, say the Rethink analysts.

PS: Do you have any questions for Aditya? Reach out to me at [email protected] and I can pass it on.

Reply