- The Conveyor

- Posts

- The Market for Greener Solar

The Market for Greener Solar

Michael Parr on China's carbon-intensive supply chain, the US's opportunity, and more.

Gowtham Ramachandran

August 30, 2024

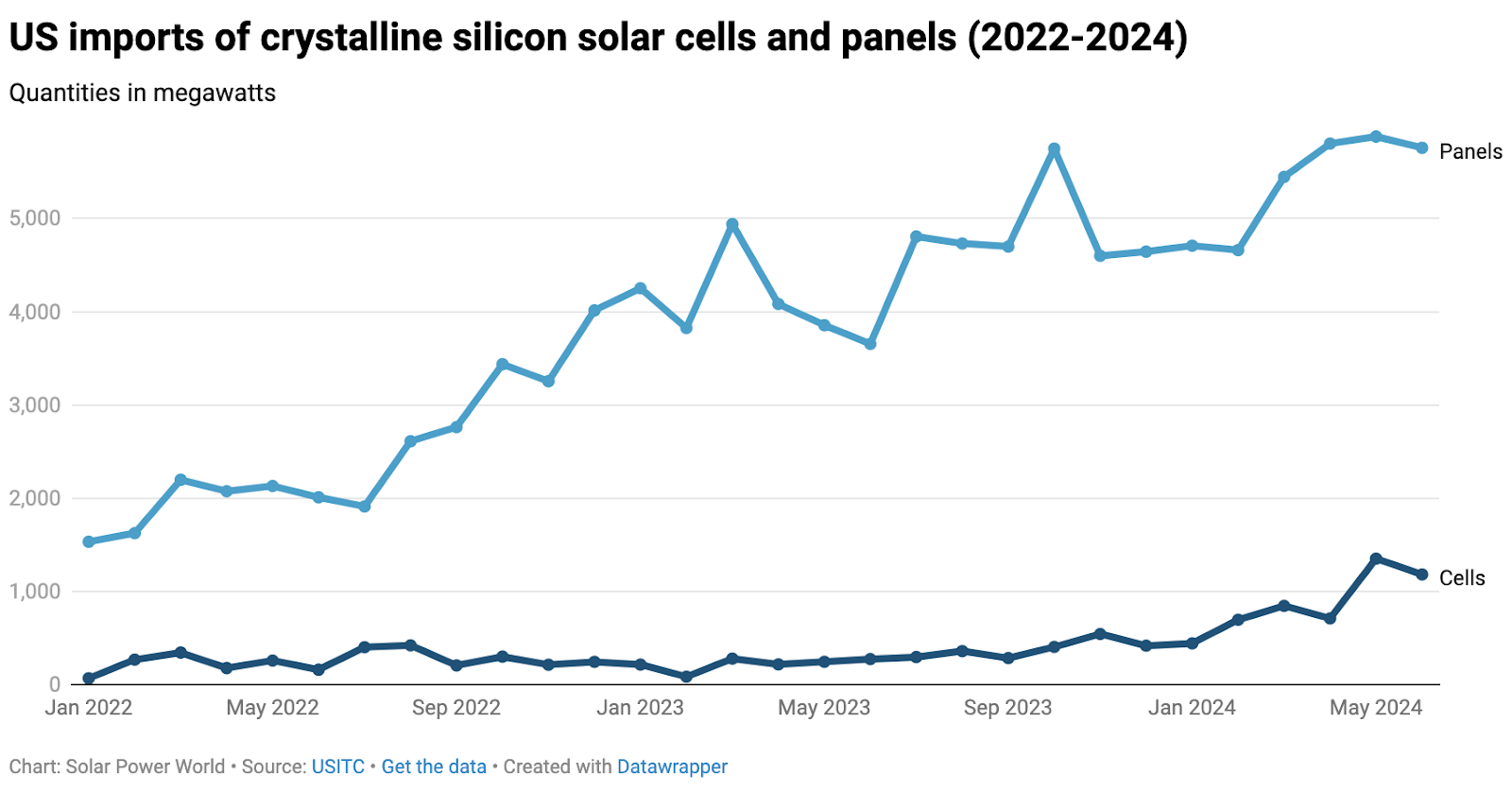

US solar manufacturers remain heavily reliant on Asia for upstream materials.

Earlier this month, the Biden Administration more than doubled the limit on tariff-free solar cell imports to help reduce costs for domestic solar panel manufacturers.

According to a White House proclamation, the tariff-rate quota (TRQ) for certain crystalline silicon photovoltaic (CSPV) cells not assembled into other products will increase from 5 gigawatts to 12.5 gigawatts.

Imports exceeding the new TRQ will continue to face a 14.25% tariff.

These tariffs were originally imposed during the Trump Administration to protect small American solar-product manufacturers from cheaper Asian imports.

In late 2023, US solar panel producers, including Hanwha Qcells, First Solar, Heliene, Suniva, Silfab, Crossroads Solar, Mission Solar, and Auxin Solar, requested an increase in the TRQ to 20 gigawatts per year.

As more domestic solar panel assembly plants come online, the demand for imported solar cells will rise until US-based solar cell manufacturing is established.

Currently, there are no domestic facilities producing solar cells, making US assemblers reliant on imports.

The policy change highlights the challenges US manufacturers will face in scaling up domestic solar production, especially given their reliance on China for upstream solar products like polysilicon, ingots, wafers, and cells.

Chart: Solar Power World

Even if the US successfully builds a domestic solar supply chain, it will struggle to compete on cost with Chinese manufacturers, who benefit from lower labor and energy expenses.

So, what’s the path forward for US manufacturers?

One approach is differentiation: targeting markets with a higher willingness to pay and developing specialized products for those markets.

One way to differentiate is by using new technologies, such as Perovskites, which can enable new applications like flexible solar cells. I recently discussed this with Aditya, who provided valuable insights into the potential of Perovskites in transforming the industry.

But the technology isn’t ready to be commercialized yet.

Another strategy to differentiate, within the boundaries of what’s possible today, is to identify a market for which there’s a higher willingness to pay and develop a product for that market.

In the US, there’s been an increasing focus on minimizing emissions across the entire lifecycle of a product, from raw material to disposal, and a push from both buyers and the government to make these products economically viable.

So, how close is the US to developing a greener supply chain?

To explore this further, I spoke with Michael Parr, Executive Director of the Ultra Low Carbon Solar Alliance, an organization dedicated to promoting sustainable practices across the solar PV value chain.

Michael shared:

Why China’s solar supply chain is carbon-intensive

Demand for greener solar products

Evolution of the US solar supply chain

Let’s dive in 👇

China’s carbon-intensive supply chain

When I asked Michael why China’s solar supply chain is so carbon-intensive, he pointed to several key factors:

China’s heavy reliance on coal to power their energy-intensive manufacturing processes.

Competitive pressures that drive cost-cutting measures, often at the expense of environmental considerations.

A relative lack of environmental regulations compared to those in Western countries.

Demand for greener products

Michael also noted that US manufacturers are increasingly starting to focus on reducing emissions in their supply chains.

The biggest competitive advantage for the US is that its energy mix, though more expensive, includes a higher proportion of renewable sources like hydro and wind. Additionally, there's a growing emphasis on using recycled materials in the upstream solar production process, which helps further reduce the carbon footprint.

Curious about the current demand dynamics, I asked Michael if buyers are showing a willingness to pay more for solar products with a lower carbon footprint.

While he acknowledged that there isn't widespread evidence of buyers willing to pay a premium yet, he highlighted a couple of market signals suggesting this trend is gaining traction.

EPEAT Eco-Label: Michael mentioned the growing interest in the EPEAT eco-label, a third-party verified standard that measures the carbon footprint of solar products. This label is becoming a key factor for buyers who want to ensure they are sourcing low-carbon solar modules, driving demand for products that meet these stringent criteria.

Carbon Border Adjustment Mechanisms: He also pointed out the potential impact of carbon border adjustment mechanisms, such as those being implemented in Europe and discussed in the US. These mechanisms would tax the carbon footprint of imported goods, effectively leveling the playing field for domestic producers who operate with lower carbon emissions.

Besides the trend towards adopting products with a low carbon footprint, Michael mentioned another interesting insight.

He shared that many buyers want to diversify away from their reliance on China, and believes this will be another factor driving the adoption of US-made solar products over the next decade.

Michael shared that many buyers want to diversify their reliance on China, and believes this is another factor that’ll drive adoption of US-made solar products over the next decade.

What’s next

Looking ahead, Michael believes that within 8 to 10 years, the vast majority of the major components needed to produce a solar module in the US will be available domestically. However, he expects challenges in areas like polysilicon and wafer production to remain.

This conversation has been edited for length and clarity.

What are the key upstream materials in the solar supply chain that US manufacturers currently rely on importing from China?

Michael Parr: The solar industry is incredibly dynamic.

About 12 to 15 years ago, it was a small specialty industry, primarily in the US, Germany, Japan, and South Korea. China saw the potential and made a strategic move to dominate solar manufacturing through their industrial policy. This shift led to a highly concentrated supply chain, where almost any product needed to make a solar module was sourced from China.

Today, most solar module manufacturing takes place in China. While there's been some diversification due to concerns over forced labor, high carbon emissions, and trade tensions, the majority of upstream components like silicon wafers, cells, and backsheets are still imported from China.

Are there any specific upstream materials that are seeing a resurgence in US production?

Michael Parr: The single biggest choke point is silicon wafers. We have three domestic polysilicon producers, but they are at full capacity. While there is some solar cell manufacturing in the US, the wafer production is still lagging.

China's overcapacity in wafer production—about 50% of global demand—leads to price suppression, making it difficult for US manufacturers to compete.

Another surprising bottleneck is glass. Although it's relatively easy to produce, glass plants are capital-intensive, and the market hasn't yet justified new capacity here in the US. Companies are beginning to see enough market potential to justify new glass plants, including innovative approaches like using recycled glass for solar applications.

But overall, the supply chain is still racing to catch up, especially in these critical upstream components.

Can you discuss how US manufacturers think about the carbon footprint of their upstream suppliers? Is this a factor in their decision-making process?

Michael Parr: For some manufacturers, it definitely is. Five years ago, there was little awareness of this issue, but it has grown significantly. The upstream elements of solar, like polysilicon and wafers, are very energy-intensive.

In China, these processes are concentrated in coal-rich areas, leading to high carbon emissions.

In contrast, US production tends to be located near hydro power or grids with a high level of renewables, resulting in a much lower carbon footprint.

This difference is increasingly important to manufacturers who want to offer a more sustainable product and to buyers who are prioritizing low-carbon options. We’re seeing more demand for low-carbon wafers and polysilicon, especially from Western producers like Norsun in Norway, which uses hydropower to minimize emissions. The focus on reducing carbon footprints is driving a shift toward these more sustainable options.

Are there new pricing mechanisms or business models emerging due to low-carbon supply chains? How do they compare with traditional supply chains?

Michael Parr: We’re starting to see new pricing mechanisms and business models emerge as a response to the demand for low-carbon supply chains, though the changes are gradual.

Historically, the solar industry has been heavily focused on cost, with Chinese manufacturers setting the benchmark through aggressive pricing. However, as awareness of the environmental impact grows, there’s a shift toward valuing sustainability alongside cost.

In the US, we’ve always had a higher-cost solar market compared to Europe, partly due to higher labor and energy costs. Domestic manufacturers who can demonstrate a low carbon footprint are beginning to find that they don’t need to charge a premium over other domestic producers, even though they may still be more expensive than Chinese imports.

One example of this shift is the EPEAT eco-label, which is gaining traction among buyers looking for modules that meet stringent carbon footprint standards.

Additionally, there’s growing interest in carbon border adjustment mechanisms, which are being implemented in Europe and discussed in the US. These would essentially tax the carbon footprint of imports, leveling the playing field for domestic producers who operate with a lower environmental impact.

How do you see the upstream solar supply chain evolving over the next decade?

Michael Parr: Currently, I would estimate that around 20-25% of the materials for US-assembled modules are sourced domestically, with the rest being imported.

Over the next five years, I expect manufacturing capacity for module assembly to triple and for upstream components to at least double.

In 8 to 10 years, I believe the vast majority of the major components needed to produce a solar module in the US will be available domestically.

However, the biggest challenges will remain in areas like polysilicon and wafer production, where the economic pressures are most severe. As the US continues to decouple its supply chain from China, the economics of these investments should improve, making it more feasible to produce these critical components domestically.

Are there any new technologies or innovations that could drive significant change in solar?

Michael Parr: I think the story of PV will be one of ongoing incremental improvement, particularly with technologies like perovskites, which have the potential to significantly increase efficiency.

However, the area that could see the most dramatic changes is energy storage, especially battery technologies. Current technologies rely heavily on minerals like lithium and nickel, but there's a lot of work being done on simpler, more sustainable battery technologies that could revolutionize energy storage.

PS: Do you have any questions for Michael? Let me know at [email protected] and I can pass it on.

Reply